Production data lags two months. Workforce surveys arrive quarterly. Yard utilisation hides inside private financials. To read the state of Malaysia’s offshore sector in any given quarter, you have to assemble five or six datasets and cross-reference them. This is the first instalment of MarineCraft Journal’s Quarterly Read.

Malaysia’s offshore industry rarely shows its hand all at once. Production data lags. Workforce surveys are quarterly. Yard activity hides inside private financials. To read the state of the sector, you have to assemble half a dozen datasets and cross-reference them. That is the work of this piece, and it is the work we intend to do every quarter.

The Quarterly Read draws on the Department of Statistics Malaysia (DOSM), the U.S. Energy Information Administration, OpenDOSM external trade releases, and Petronas’s published Activity Outlook to picture where Malaysia’s upstream and offshore-services sectors actually stand. We focus on signals that matter for operational decisions. Are operators expanding or holding? Is the workforce tight or slack? Where is the fab pipeline pointing?

The headline read for Q4 2025 and early 2026: the picture is quietly tightening. Output per worker in mining is rising while headcount holds flat. Net mineral fuel exports are widening sharply as imports fall. Fabricated metal output is up. The labour market, already at 3.0% unemployment, has no slack to give. And Petronas’s freshly-published 2026-2028 Activity Outlook signals continued upstream activity through the end of the decade. None of these signals point in opposite directions, which is itself the story.

The signal in brief

- Production. IPI Mining at 98.5 (March 2026), down 6.5% year-on-year but with a clear up-trend over the latest six months relative to the prior six. Output per worker up 2.0%, employment effectively flat. Productivity widening.

- Trade. Mineral fuel exports up 4.6% YoY in March 2026, imports down 20.0%. Net trade balance widened to RM 4.97 billion in a single month. The export-import gap is opening, not closing.

- Yard, workforce, capex signal. IPI Fabricated Metal at 146.8, up 4.0% YoY, the seventh consecutive month above 140. National unemployment 3.0%, participation 70.9%. Petronas committed to sustaining ~2 million BOED through 2028.

Production: how is the upstream physically moving?

Mining-sector output, as measured by Malaysia’s Industrial Production Index for the B.06 division (crude oil and natural gas), stood at 98.5 in March 2026. That is down 6.5% year-on-year, but the 12-month trend (last six months versus prior six) is up. Translation: a weak patch in mid-2025 is still sitting in the YoY denominator, while the underlying direction has improved.

The more interesting number sits inside the labour data. Productivity in the mining sector, measured as output per worker in constant 2015 ringgit, was RM 346,468 in Q4 2025, against RM 339,714 four quarters earlier. Up 2.0%.

Mining sector employment, meanwhile, was flat. 77.0 thousand persons in Q4 2025, identical to Q4 2024 to one decimal place. Output per worker rising while headcount holds is a textbook productivity-divergence pattern, with two plausible explanations. Either operators are extracting more from existing crews (capacity discipline rather than expansion), or the talent pool is too tight to add bodies even where the work justifies them. Both readings are operationally meaningful, and they are not mutually exclusive.

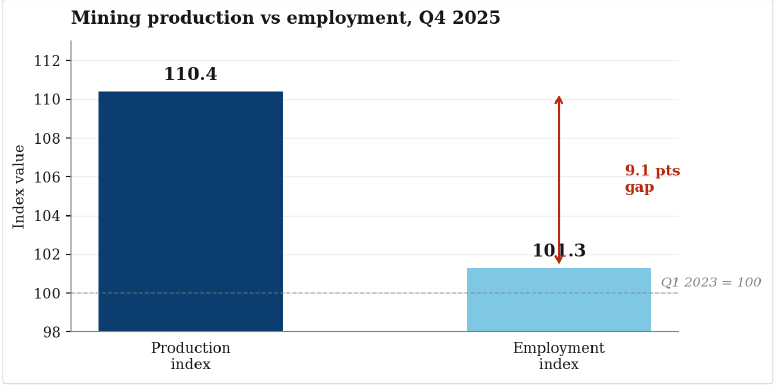

A nine-point production-to-employment gap historically precedes upward pressure on skilled-trade wages by six to nine months.

When we index both series to a common base (Q1 2023 = 100), the production index sits at 110.4 against an employment index of 101.3. A nine-point gap, widening, with the production line clearly above. In Malaysian mining data, this configuration historically precedes upward pressure on skilled-trade wages by six to nine months. We will come back to this in §3.

Workforce: tightening or loosening?

The labour-force survey for Q3 2025 (the most recent release) shows the macro picture. Total employed at 16.97 million persons. Unemployment at 3.0%. Labour-force participation at 70.9%. Employment-to-population ratio at 68.8%. By any of these measures, Malaysia’s labour market is tight.

Drilling into the mining-specific picture, the most recent published median wage figure for the formal-sector Mining and Quarrying category sits at approximately RM 8,800 per month (DOSM Salaries and Wages of Paid Employees, March 2025 reference data). That makes mining the highest-paying sector in Malaysian formal employment, despite representing only around 0.6% of the national workforce.

Read this against §2. Rising productivity. Flat headcount. Already-tight macro labour market. Highest sector wage in the country. None of these signals point to abundance. For operators planning new mobilisations, for EPCIC contractors planning bid posture, and for service companies budgeting 2026 wage reviews, the workforce signal is the same: skilled trades will not get cheaper or easier to find.

Trade flows: is petroleum still pulling its weight?

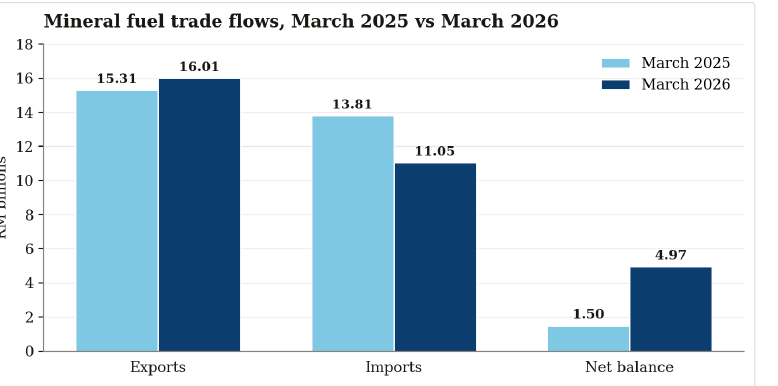

Mineral fuel exports (SITC section 3, covering crude petroleum, refined products, and LNG) totalled RM 16.01 billion in March 2026, up 4.6% year-on-year. Imports for the same category came in at RM 11.05 billion, down a striking 20.0% YoY. The net trade balance: RM 4.97 billion in mineral fuel surplus, in a single month, with the gap widening as imports fall faster than exports rise. (DOSM flags the most recent two months as provisional, so we will watch for revisions.)

There are two ways to read the import-side drop. The bullish version: domestic refining and downstream demand are moderating, while upstream production maintains or grows. The cautious version: a falling import bill can also reflect inventory destocking or lower refinery throughput, neither of which is a structural positive. Without a parallel read on Pengerang utilisation and refinery margins, we cannot fully separate the two stories.

The export side of the picture is consistent with the production data. Volumes are holding or rising, and the world is buying.

What we can say: the export side of the picture is consistent with the production data in §2. Volumes are holding or rising, and the world is buying. For the offshore-services sector that depends on operator capex following revenue, this is a positive demand signal, provided the price environment does not crater between now and the next outlook update.

Yard signals: where is the fab pipeline?

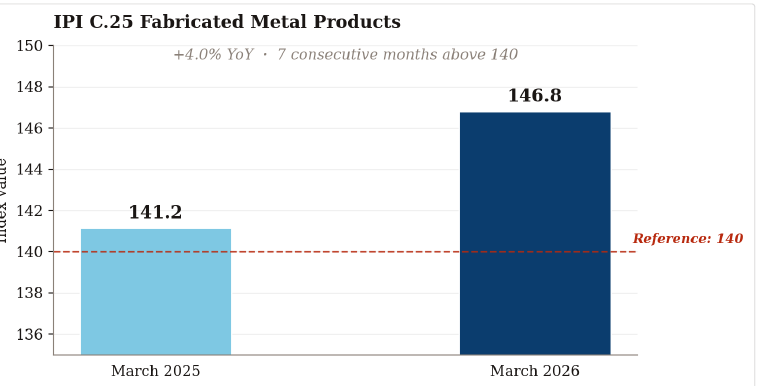

The closest public proxy for Malaysian offshore yard activity is the IPI division C.25, Manufacture of Fabricated Metal Products. The category covers fabrication output across all of Malaysian manufacturing, not just offshore yards, but yards (MMHE Pasir Gudang, Sapura Lumut, smaller specialist shops) are the largest concentrated employer in the category, and the index moves with their order books.

C.25 stood at 146.8 in March 2026, up 4.0% year-on-year, with the 12-month trend pointing up. That is the seventh consecutive month above the 140 mark, a level last seen consistently in mid-2023. The trend is not dramatic, but it is monotonic and broad-based.

Our internal manual yard tracker (MMHE quarterly revenues, Sapura Energy, Bursa O&G index) does not yet have entries logged for this period, so we are holding off on operator-specific commentary in this instalment. Once those entries populate, future Quarterly Reads will overlay peer revenue against the C.25 signal. Divergence between fab IPI and named-operator revenues usually points to share-loss or project-cycle questions worth asking. For now the read is straightforward: fabrication output is up, trending up, and consistent with an upstream demand environment that is adding rather than shedding work.

The Petronas overlay

The picture above sits on top of Petronas’s own forward plan. The PETRONAS Activity Outlook 2026-2028, released on 29 January 2026, signals continued upstream activity through the end of the decade. Three points stand out for OGSE planners.

First, production targets. Petronas plans to sustain Malaysia’s oil and gas production at approximately 2 million BOED through 2028, supported by exploration, deepwater developments, and enhanced oil recovery (EOR) at producing assets including Belud, Sepat, and Kurma Manis. This is a sustain-and-optimise mandate, not an aggressive expansion target.

Second, Gas and Maritime emphasis. Fleet rejuvenation, lower-emission shipping investments, and continued LNG portfolio development are explicit priorities, relevant for operators of OSVs, LNG carriers, and bunkering services positioning for the next contracting cycle.

Third, downstream timeline. A new Petronas biorefinery is targeted to commence operations in the second half of 2028, with operational excellence and supply chain resilience flagged as priorities amid persistent margin pressure. For specialty-chemicals and biofuels-adjacent vendors, the calendar is set.

Short version: Petronas is signalling a sustained upstream activity floor for the next three years. Combined with the production and trade data above, the message is internally consistent. Capacity will be maintained, and OGSE companies should plan for sustained rather than accelerating demand.

The strategic read

Operators

The picture supports holding rather than aggressive expansion. Production is rising per worker but volume is recovering, not surging. The Petronas signal is “sustain 2 million BOED,” not “grow it.” Tempo, not breakout. Capex discipline remains the operating posture.

EPCIC and fabrication contractors

The C.25 fab metal trend is encouraging. Output sits at multi-year highs, and Petronas’s continued deepwater development commitment maintains the EPCIC pipeline. Bid posture should reflect a market that is working, not flooded with cheap capacity but not desperate for any project either.

Hiring and training

The writing is on the wall. Mining wages are already the highest in the country. Labour-force participation is near record. Sector employment is flat in the face of rising productivity. Companies budgeting on 2024 wage assumptions for 2026 hires will miss. Recruitment lead times will lengthen if upstream activity ticks up further.

Pricing power

The productivity-to-employment divergence is the signal to watch. When output rises faster than headcount over multiple consecutive quarters, sector wages typically follow within six to nine months. Contractors with skilled-trade payrolls get squeezed unless rate cards keep pace. Expect pressure on EPCIC unit rates and OSV day rates over the next two to three quarters.

Investors

The trade balance widening, the fab metal trend, and the Petronas sustained-production signal together form a quietly constructive combination. Not breakout territory. But no obvious slack either. For Malaysian OGSE-exposed positions, the macro tape is supportive without being euphoric.

What we will watch next quarter

Will the productivity-to-employment divergence narrow, widen, or stabilise?

Q1 2026 productivity data drops on 21 May 2026. If the gap continues to widen, the wage-pressure thesis strengthens. If it narrows, the read is operators starting to add headcount, an early sign of expansion intent.

Will the mineral fuel net export gap continue to widen?

The import-side drop is the variable to watch. If imports stabilise or recover while exports hold, the gap narrows and the demand picture clarifies. If imports continue falling, the structural-versus-destocking question becomes pressing.

Will IPI C.25 hold above 140 for an eighth consecutive month?

A break below 140 would be the first negative signal in this quarter’s read. A continuation above 145 would confirm the fab-output uptrend and align with the Petronas EPCIC commitment.

Production (§2): IPI Mining division B.06, monthly (DOSM, OpenDOSM via storage.dosm.gov.my). Productivity_qtr filtered to Mining and quarrying (sector code p2, DOSM Labour Productivity Statistics, quarterly, in constant 2015 prices).

Workforce (§3): Quarterly Labour Force Survey lfs_qtr (DOSM). Median wage figure from Salaries and Wages of Paid Employees publication (DOSM, March 2025 reference data; figure is published as a PDF rather than a structured dataset).

Trade (§4): External Trade by SITC section 3, Mineral fuels lubricants and related materials, monthly (DOSM trade_sitc_1d). Most recent two months are provisional per DOSM caveats.

Yard signals (§5): IPI division C.25, Manufacture of Fabricated Metal Products (DOSM, monthly).

Petronas overlay (§6): PETRONAS Activity Outlook 2026-2028, published 29 January 2026 (Petroliam Nasional Berhad press release and document).

All figures sourced as of 9 May 2026. Charts are endpoint comparisons compiled by MarineCraft Internal Intelligence; full monthly trend visualisations will accompany future instalments. Subsequent revisions by DOSM may apply, particularly to provisional months.

Sources: DOSM (productivity_qtr, lfs_qtr, trade_sitc_1d, ipi_2d) · DOSM Salaries and Wages publication (March 2025) · PETRONAS Activity Outlook 2026-2028 (29 January 2026) · World Oil, “PETRONAS outlines upstream investment plans through 2028” (30 January 2026)